Share

Copied

Editor's note: Gunter Schoech is a German entrepreneur, founder and managing director of Débrouillage Ltd., a Sino-German market intelligence consultancy. He writes on Sino-Western relations and macroeconomics. The article reflects the author's opinions and not necessarily the views of CGTN.

One might feel like the little boy in the fairytale “The emperor’s new clothes” looking at our global monetary system: It is inherently unstable, yet few even expose the situation for fear of the consequences, let alone take action. There is rather forced optimism, the willingness to ride the wave as long as it lasts, and modern monetary theory even attempts an academic underpinning why this time it’s different.

Since the 2008 debt crisis, according to the Bank of International Settlements, the sum of private, corporate and national debts has risen globally by 50 percent to 400 percent in China.

Lehman Brothers 2008 had 35 trillion U.S. dollars of notional derivatives causing the ripple effect. Deutsche Bank, fighting for survival 2019, has 56 trillion U.S. dollars.

Derivatives are speculative bets on the performance of an “underlying,” e.g. an asset, index, or interest rate. About 90 percent are negotiated directly between two parties, making them largely unregulated. Nobody even knows the exact volume and notional estimates go beyond 1000 trillion U.S. dollars globally. For comparison: World GDP stands at 80 trillion U.S. dollars, according to the World Bank.

Derivatives are in Warren Buffett’s words “weapons of mass destruction that morph, mutate, and multiply until some event makes their toxicity clear.” They tie financial institutions to each other, enabling a chain reaction.

What still holds things together are artificially low or zero interest rates. Historically, in a bull market, interest rates were brought back up by 4 to 5 percent as minimum ammunition to counter the next crisis. This time, the U.S. central bank failed not even halfway. The European central bank hasn’t even tried.

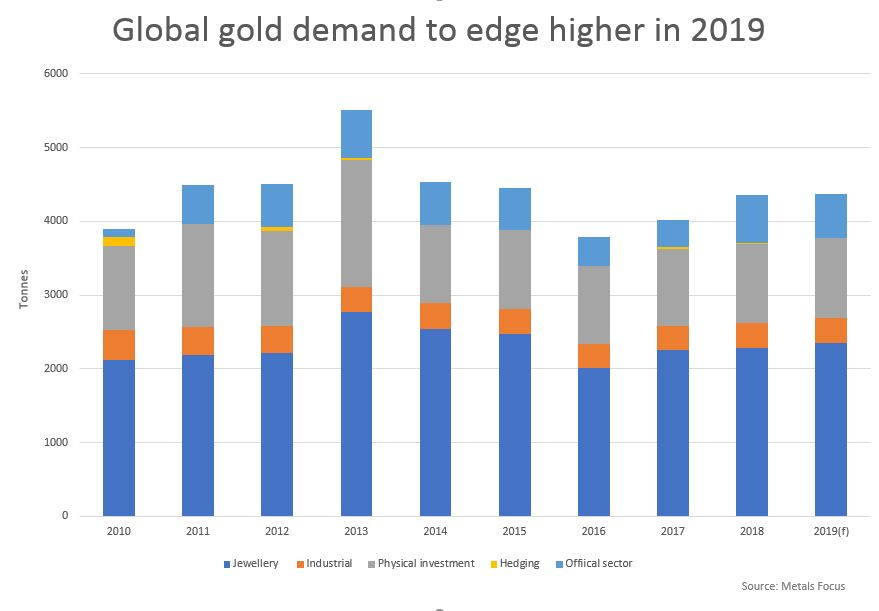

Gold demand between 2010 and 2019. /Reuters Photo

Low interest rates are like taking drugs, making most feel better in the short run, but with terrible side effects and payback time: Bad companies stayed in business, commercial banks’ business models are destroyed (part of Deutsche Bank’s problems), consumers load up on home-, car- credit card- or student loans, and central banks must buy up government- and even corporate debt because the free markets won’t. Other solutions are deeply unpopular like expense cutting, controlled defaults and significant redistribution of wealth.

If the world had been willing to reset the system to a sound basis, it would have done so in 2008. Instead, it printed at record levels to patch over 2008. Now we are beyond the point of no return. U.S. national debt grows faster than U.S. GDP and is 182,000 U.S. dollars per taxpayer; unfunded liabilities several times that. Personal debt per citizen is another 60,000 U.S. dollars.

Obviously, such debts can never truly be paid back, only if devalued.

Today’s paper money is backed by nothing but faith in its value, which can be lost as quickly as in the fairy tale. Latin fiat means "let it be done": Governments only decree that an intrinsically valueless object is legal tender.

Good, trustworthy money needs limited supply. Precious metals were the money of choice for thousands of years.

Paper fiat currencies are in unlimited supply if the government chooses, and thus can fail as a store of value; politically independent central banks should restrain governments which historically always lost discipline eventually.

In 2019, President Trump threatened to fire his own nominee as Federal Reserve Chairman, Jerome Powell, if he does not cut interest rates. Turkey’s president Recep Tayyip Erdogan reportedly fired his central bank chief.

VCG Photo

Countries around the world prepare for the time when the US dollar as the single reserve currency will end. Officially, they usually deny that gold is money. But in 2018, the volume of gold bought by central banks rose to its highest level since the end of the partial gold standard 1971.

Historically, France, Italy and Germany have about 60 to 70 percent of their foreign reserves in gold, and made sure to repatriate them from the U.S., also not exactly a sign of trust.

China’s foreign reserves at 3 trillion U.S. dollars are the largest in the world, thereof only 2.5 percent gold. It has unusual incentives to change this: About 60 percent of its reserves are in U.S. dollar-denominated Treasury bonds, a result of cumulated trade surpluses. This gives China a terrible trade war weapon of last resort: How could the U.S. sell new debt, which it must at its 5 percent budget deficit, if the market is flooded by China?

However, falling prices would hurt China too. So China has stopped to renew mature bonds and buy U.S. dollar-denominated gold instead in December 2018 after a two-year pause.

China prepares for a world with an increasing trade outside the U.S. dollar. Long term, it seeks to establish the yuan as a sound currency, somehow linked to gold. Official holdings of gold have more than tripled since 2008, and given imports and China being the largest miner are probably much higher.

Other states aggressively follow a similar path, e.g. Russia quadrupled its gold in a decade. Today, about 60 percent of global foreign currency reserves and global transactions are in U.S. dollars. China and Russia happen to be the two nations which have by far concluded the most and largest bilateral trade agreements abandoning the U.S. dollar. In years or decades, payment system alternatives to SWIFT and cryptocurrencies for convenience, but with a periodical account balancing between nations through the transfer of physical gold, could lead to a new, sound monetary system.

No emperor has ever looked naked in over 5,000 years if he possessed gold.

(If you want to contribute and have specific expertise, please contact us at opinions@cgtn.com.)