- Home

- China

- World

- Europe

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

Share

Copied

Editor's Note: Jimmy Zhu is chief strategist at Fullerton Research. The article reflects the author's opinion, and not necessarily the views of CGTN.

The U.S. Federal Reserve signaled that it will pause the rate cuts for some time in its overnight policy meeting, a move that is considered as hawkish. Surprisingly, the dollar slumped while U.S. stocks gained.

The Federal Open Market Committee (FOMC) met in September, indicating that the labor market remains strong and economic activity has been rising at a moderate rate. Most importantly, the Fed's statement dropped the language that it will "act as appropriate to sustain the expansion," and Powell said the monetary policy is in a good place. At the press conference, Powell said the risks to the growth outlook is more balanced at this moment compared to past months, due to reduced uncertainties from U.S.-China trade talk progress and Brexit development.

Dollar weakening even as Fed signaled a pause in rate cut

The greenback rose initially after the Fed's statement, as investors were caught up with the hawkish language in the statement and Powell's speech. However, the gain was short-lived. The dollar index rose as much as 0.32 percent to 98.004, and fell 0.24 percent to 97.453 at closing. Not only did the U.S. dollar reflect a "dovish Fed," the stock market told a same story. Without verbal support from the Fed, S&P 500 closed 0.33 percent higher at 3046.77, and safe-haven asset – gold rallied 0.5 percent to 1495.66.

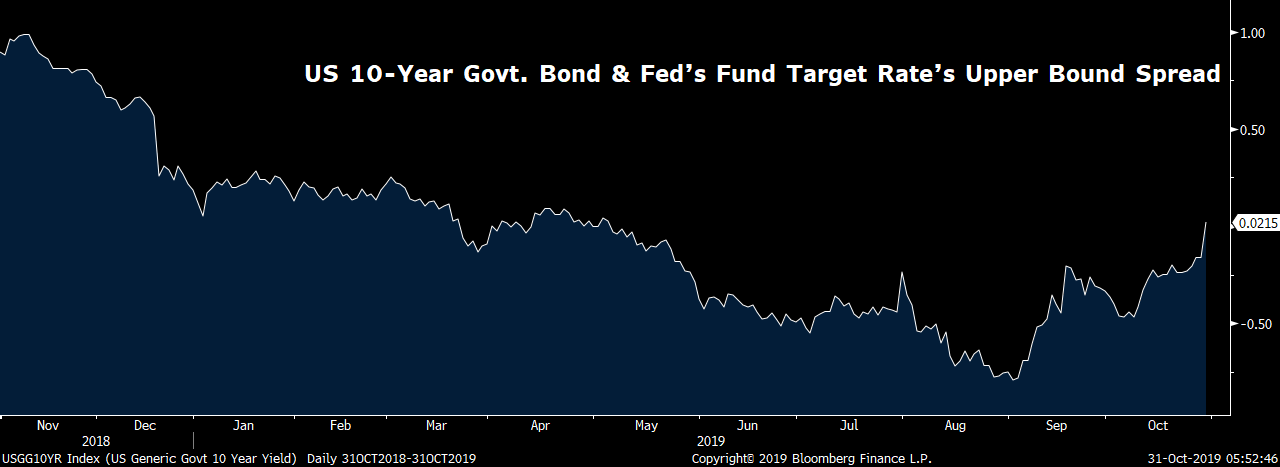

Markets are actually not wrong on the pricing if those key rates' spread has anything to say. U.S. 10-year government bond yield is now standing at 1.78 percent, edging above the Fed's fund target rate's upper bound since early May for the first time. The Fed's fund target rate's upper bound has now been reduced to 1.75 percent.

Source: Bloomberg

The 10-year government bond yield usually reflect traders' expectation on the upcoming economic and inflation outlook. When this rate is above the benchmark one, it's fair to say that there is no urgency for the Fed to further reduce the policy rate in near term. The monetary policy is loose enough to justify the current economic backdrop. In other words, the monetary policy is actually looser compared to the last five months. Current dollar index around 97.45 is similar to the level in early May, suggesting that the dollar and bond market are reflecting the same monetary condition in the U.S.

U.S. Q3 GDP data shows that a fourth rate cut in near term is not justified

Key U.S. economic data released overnight also suggests the Fed's rate cut should take a pause. U.S. GDP data shows that the economy grew 1.9 percent, higher than the earlier estimates of 1.6 percent. The surprise uptick is from consumer spending, which expanded at 2.9 percent.

Unlike the situation in the euro zone, resilient growth in U.S. consumer spending shows that the slowdown in manufacturing sectors has yet to have a negative impact on consumers' sentiment. The Fed's determination to support the economy by cutting the benchmark rate twice at 50bps may have buoyed consumers' confidence.

Also, S&P 500 index rose 1.2 percent in the third quarter despite U.S.-China trade tension. Data shows that U.S. consumer confidence index has been moving in tandem with S&P 500 stock index in the past five years.

Source: Bloomberg

In the final two months of the year, there is no sign that macroeconomic condition in major economies will see substantial changes. From the U.S.-China trade negotiation perspective, current development shows that both sides are trying to work something out and the tension will be contained in the coming months at least. The probability of a rate cut in December's meeting now stands at only 23.5 percent, according to the rates market.