- Home

- China

- World

- Europe

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

Share

Copied

Editor's Note: Jimmy Zhu is a chief strategist at Fullerton Research. The article reflects the author's opinion, and not necessarily the views of CGTN.

ISM manufacturing PMI shows that U.S. manufacturing activities slowed at a faster pace in November, raising doubts on the increasing hopes of a global economic recovery.

Stocks selloff after ISM PMI as traders downgrade their outlooks on the strength of U.S. economy

The headline ISM figure dropped to 48.1 last month from the previous 48.3, when most of the other major economies' PMIs improved in November. Also, the number has been below the key threshold of 50 for a fourth consecutive month. Global stocks quickly retreated upon the releases of the U.S. PMI figures, with Dow Jones Industrial Average sliding 0.96 percent, the biggest decline since October 2.

S&P 500 has rallied over four percent since beginning of the fourth quarter, as earlier massive central banks' policy easing and rising hopes on U.S.-China to reach some of the trade deals boost the confidence. The worse-than-expected ISM figure served as a timely reminder to those traders in the stocks market that their earlier expectations on the economic outlook could be lacking off the basis.

ISM's new export orders could be one of the most accurate indicators to reflect the global growth

ISM's new export orders fell to 47.9, after it climbed above 50 in October. The chart below shows that new export orders have been moving consistently with the global growth. However, many major economies' manufacturing PMIs reflect an improving outlook.

Source: Bloomberg

The bad news is that analysis shows that ISM's readings have been more accurate to reflect the global picture than many others. Correlation between the ISM's new export orders and the world GDP growth tracked by Bloomberg stood at 0.78 in past three years, higher than JP Morgan global PMI's correlation with Bloomberg world GDP, which is 0.68.

Baltic Exchange Dry index (BDI) shows a similar picture as what ISM's new export orders described. The index dropped 11.7 percent in November, declining for a third consecutive month. Less shipping activities seen in BDI means the global trades have been weakening amid prolonged U.S.-China trade tension.

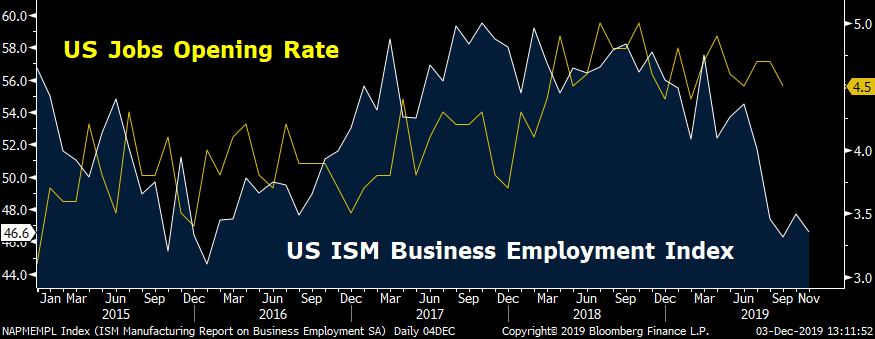

ISM manufacturing PMI may risk the Friday's jobs data to the downside

Sub-indices in PMI also declined in a broad basis. New orders dropped to 47.2 from October's reading of 49.1. The employment index has been staying below 50 for a fourth consecutive month, and the figure slowed to 46.6 in November from the previous 47.7. Lower readings in both indices suggest that the slower domestic demands may have already had some negative impacts on broader U.S. labor market.

Nonfarm payrolls in November may have increased 190,000, according to the current consensus. The estimate is much higher than the reading at 128,000 from the previous month, which contradicts what PMI employment index is showed. A chart below shows that U.S. jobs opening rate and ISM's business employment index have been moving in tandem. A slower PMI's index indicates that job vacancies include either newly created or unoccupied positions will be becoming less.

Source: Bloomberg

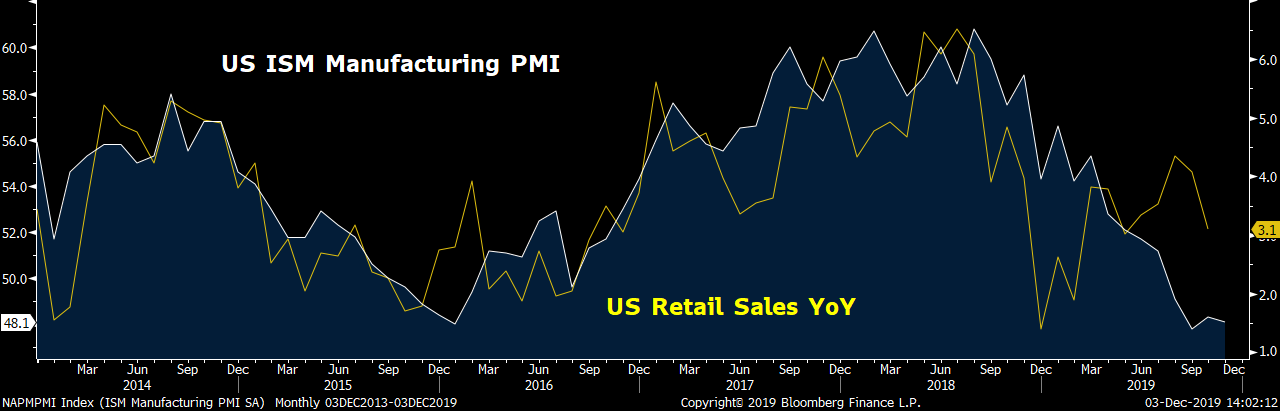

Tepid manufacturing actives will drag service sectors sooner or later

Despite U.S. manufacturing accounting for around 20 percent of its entire economy, its actual impact is much larger than the percentage number shows. Data shows the correlation between the ISM manufacturing PMI and U.S. retail sales growth stands at 0.7 in past five years. Retail sales account for about 70 percent of the entire country's growth. A high correlation figure means slow U.S. manufacturing activities have direct impact on the broader U.S. economy.

Source: Bloomberg

The growth for U.S. economy this year is largely supported by the strong consumption. However, manufacturing PMI readings persistently below 50 will spread into service sectors sooner or later, because many of the service-related activities are associated with the relevant manufacturing growth.

The non-manufacturing PMI to be released on Wednesday will be crucial. For now, market still expects a modest rise from the reading at 54.5 in October. However, if the actual reading misses the expectations, we might see another round of large selloff in the U.S. stocks market. If that happens, the pressures on Fed to cut rate again would return soon.