- Home

- China

- World

- Europe

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

Share

Copied

Editor's Note: Jimmy Zhu is chief strategist at Fullerton Research. The article reflects the author's opinion, and not necessarily the views of CGTN.

Gold is one of the best performers compared to other major assets this year, largely due to flows into safe-haven territory in earlier quarters due to China-U.S. trade tensions. However, its prices are surprisingly holding steady this week confusing many investors, while stocks traders are busy celebrating the developments in trade negation.

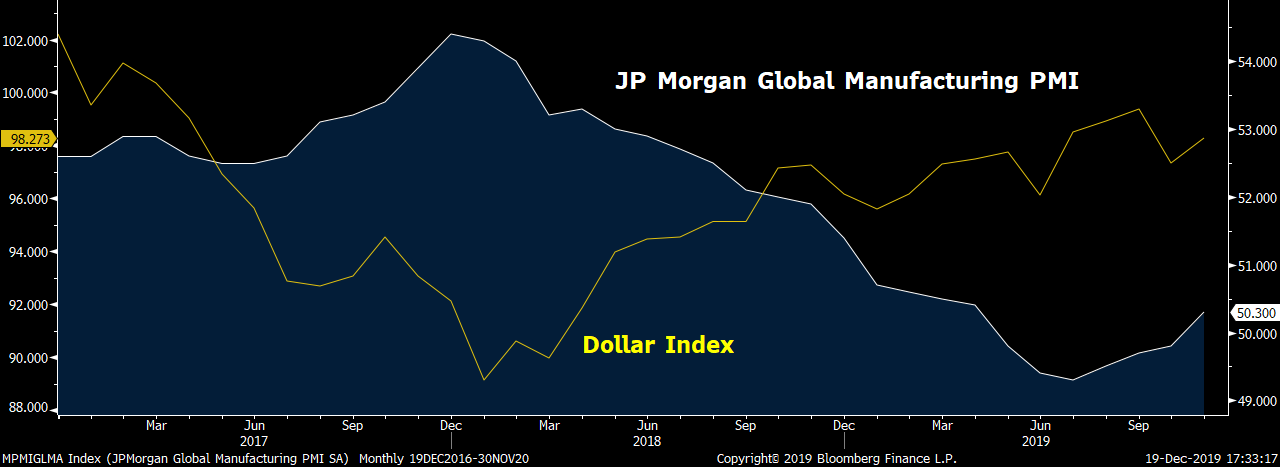

Gold price reflects the perception of dollar's upcoming downtrend

The recent stability in gold prices reflects the markets' expectations on a weaker dollar in the coming months, supporting the yuan outlook. Historically, the gold and dollar's trend have tended to move inversely, and sometimes it's not easy to explain who leads the other.

If traders believe the greenback is going to depreciate as a general rule, sometimes they would express their opinions and sentiment on the dollar through buying gold, instead of selling the dollar index. The reason is there are different currencies in the dollar index, such as the euro, yen, etc. For example, if the euro and yen are heading in a different direction due to ECB (European Central Bank) and BoJ (Bank of Japan) policy divergence, the dollar index could end up unchanged. Thus, the dollar index is not able to reflect the sentiment on the greenback sometimes.

After recent global economic data showed signs of improving and the easing of trade tensions between the two largest economies, many investors see little reason for the dollar, which is one of the key safe-haven currencies, to further appreciate after it gained 3.4 percent in the third quarter. Though many economists point out that the global economy will remain fragile in 2020, positive developments in the China-U.S. trade negotiation and Brexit are more "eye-catching" to traders.

Gold's stability seen as positive sign to Shanghai stocks

A chart below shows that the gold price has been surprisingly moving in the same direction with the Shanghai composite index in the past two years. It's very difficult to apply most of the fundamental theories to explain such a price relationship. However, if gold's move is a reflection on dollar sentiment, then it makes sense.

Source: Bloomberg

One of the main reasons for increasing bearish bets on the dollar is that those economies outside of the U.S. are expected to outperform in 2020, after fading trade tension and Brexit risks. If this prediction is accurate, it will largely boost the Chinese exporters' outlook in 2020. It is noted that China exports to the U.S. account for only around 20 percent of its total outbound shipping activities, so the growth recovery outside the U.S. will be more important to Chinese exporters' outlook.

There is also visible evidence to prove that the dollar's performance has been usually inverted with global economic activities. A graph below shows that these two have been always moving in the opposite direction in the past three years, and their negative correlation held at 0.62 in this period. Having said that, when gold's stability reflects a weaker dollar outlook, investors expect the global economy to recover simultaneously.

Source: Bloomberg

A chart below shows that Chinese export orders have a substantial impact on the local stock market. The PMI export orders index and Shanghai stocks quickly rebounded at the beginning of the year and both gradually recovered in the middle of the third quarter after sharp declines in the second quarter. Correlation between the two stands at 0.68 in the past three years, the regression model shows that the Shanghai composite index may rise toward 3,115 assuming that the China new export orders PMI returns to the 50-level threshold. The stocks index closed at 3017 as of December 19.

Source: Bloomberg

Gold price predicts that central banks' stimulus is not yet over

Gold's stability reflects markets' expectations on central banks' monetary policy outlook as well. When markets expect the central banks to ease the monetary policy, gold has been consistently outperforming most of the other major assets in the world. For example, when the Fed started cutting the policy rate in 2001, gold reversed its declines in the past five years and gained 2.46 percent on that year; the Fed implemented its historical QE after the global financial crisis in 2008, gold rallied over 100 percent in the next few years. Global central banks have cut the policy rates over 50 times this year and gold has rallied over 15 percent, heading to the best year since 2010.

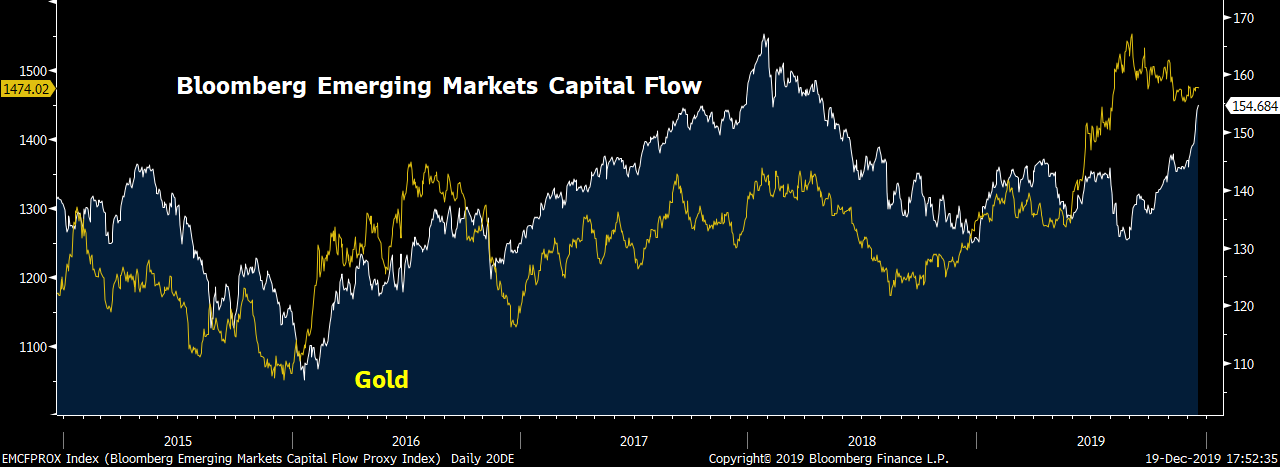

Even with synchronized rallies in global stocks in the past few days after some key risks had been removed, gold prices are staying where it was at the end of last week. Thus, the other explanation in gold's stability is likely due to the expectation of continued monetary easing by central banks. A chart below illustrates that capital flows into the Emerging Markets have been consistently moving together with the gold prices in the past five years. This is because when central banks release the liquidity, capital flows usually prefer those markets offering the higher yield, emerging markets become a "sweet spot."

Source: Bloomberg

China is the biggest economy in the emerging markets, and its interest rate spread with many other major economies, including the U.S., is widening. When a large amount of capital flows move into the Emerging Markets, the Chinese capital market would be a large beneficiary.