- Home

- China

- World

- Europe

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

Share

Copied

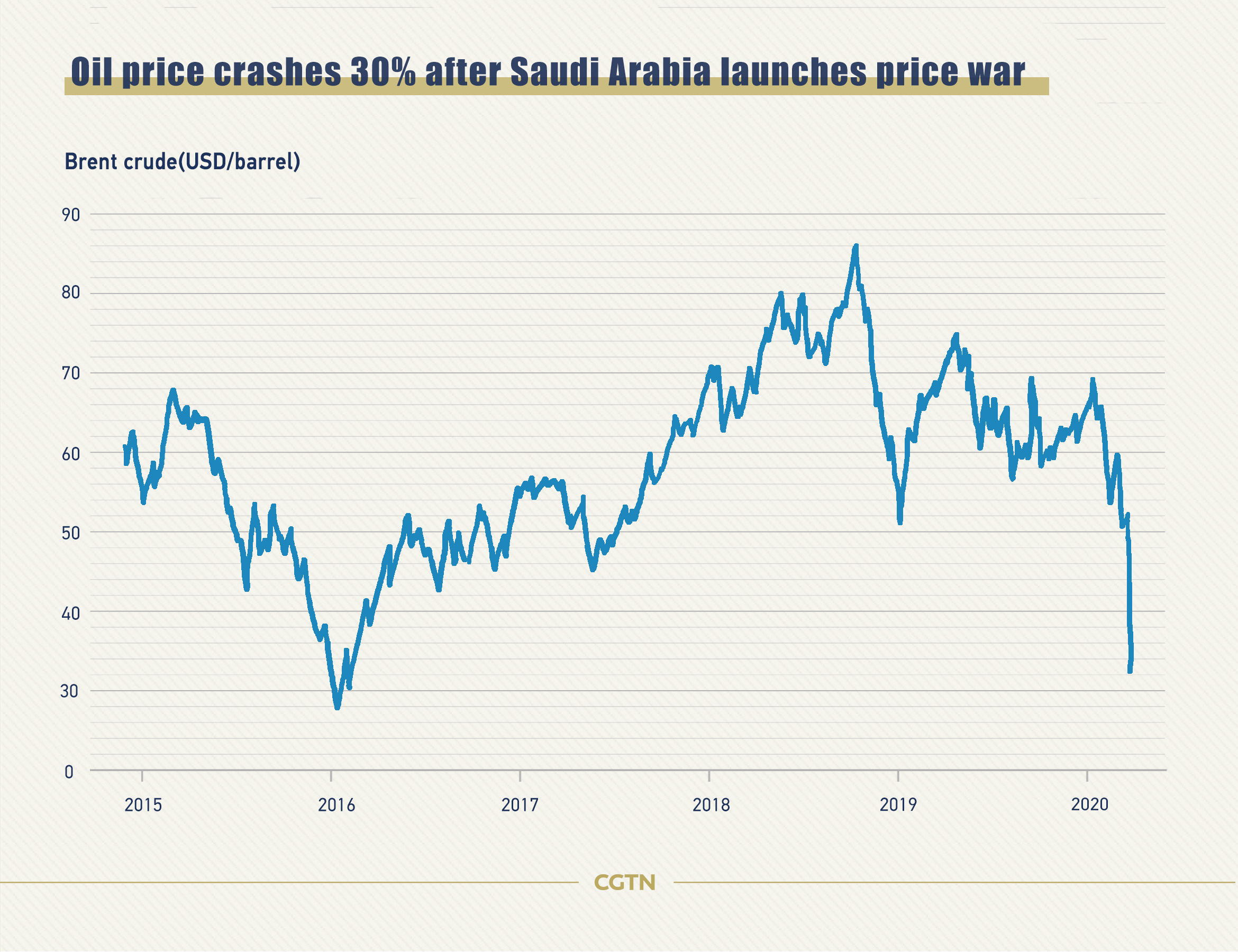

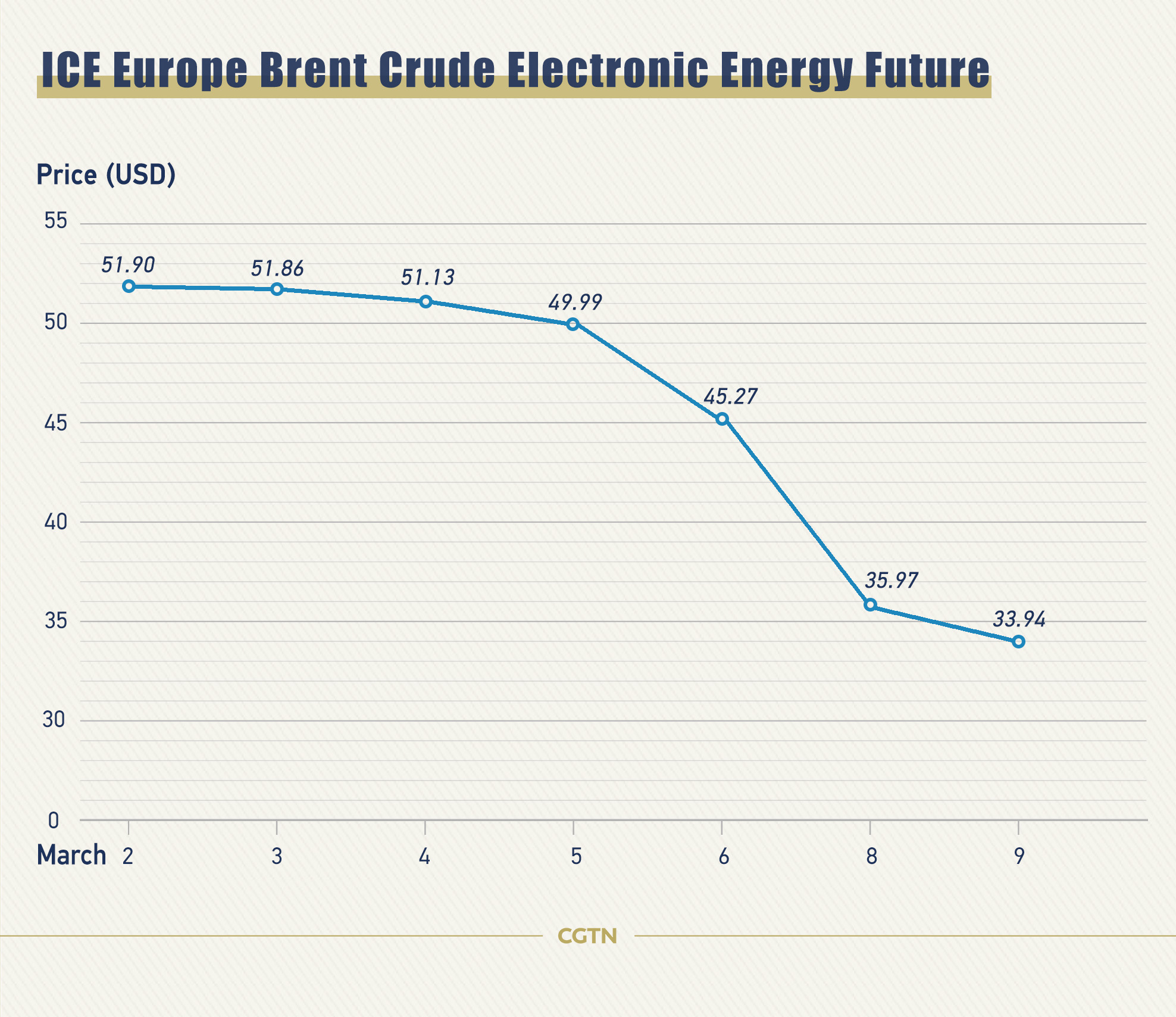

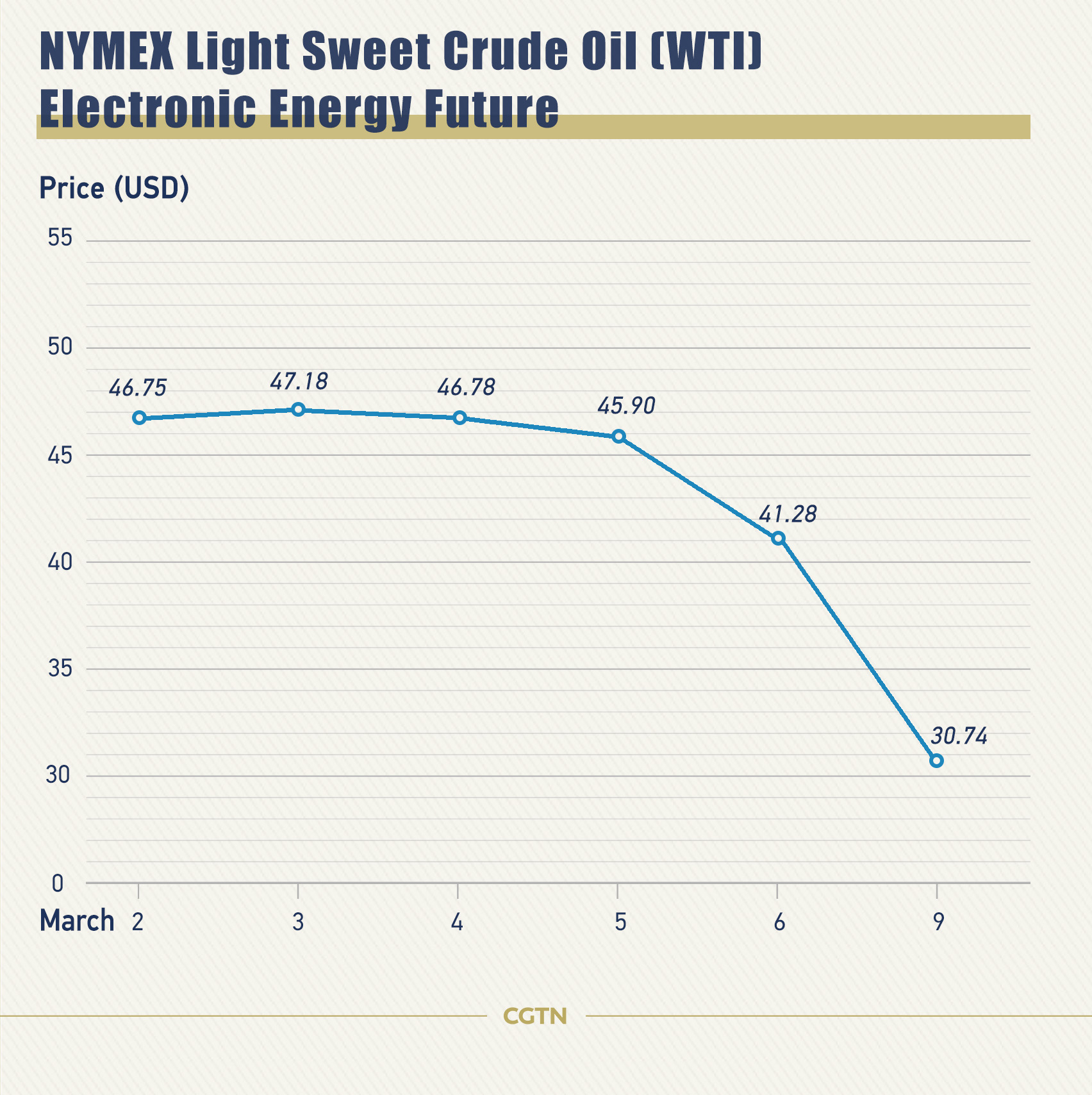

Oil prices crashed on Monday after Saudi Arabia slashed its official selling price, adding uncertainty to a world economy that continues to struggle with COVID-19.

The Saudi's national petroleum Saudi Aramco reportedly plans to raise its production significantly after OPEC's failure to strike a deal with its allies regarding production cuts, giving rise to fears that tensions between oil producers will exert more pressure on prices. The world's top oil exporter's discount has embroiled other oil providers in a "price war."

Crude plummeted more than 30 percent at a time, marking the hardest drop since the Gulf War in 1991. As of 5:15 a.m. GMT, WTI Crude plunged 31.08 percent and Brent Crude was down 28.50 percent.

According to Bloomberg citing people familiar with the conversations, "Saudi Arabia has privately told some market participants it could raise production much higher if needed, even going to a record 12 million barrels a day."

"The plunge of the oil price is predictable," Shanghai Petroleum and Natural Gas Exchange's Index R&D Department Senior Supervisor Sero Qu told CGTN. He continued explaining that the last major oil price plunge in late 2014 was also caused by the failure of OPEC's production cuts deal.

"The main reason for the price drop is in the supply side," Qu said. Even though the coronavirus outbreak has an impact on the oil market, the demand is still solid after the central banks got into easing mode.

"And that is why Russia doesn't want to cut the production with Saudi Arabia," added Qu. "They think the coronavirus impact is temporary, and they don't want to lose market share by cutting the production."

Participants attend the official ceremony marking the debut of Saudi Aramco's initial public offering (IPO) on the Riyadh's stock market, in Riyadh, Saudi Arabia, December 11, 2019. Marwa Rashad/Reuters

Qu believes oil prices have not yet touched bottom since history has shown that prices can go down 50 to 60 percent.

From a short term perspective, Qu expected the oil prices would tumble due to the effect of this price war, but he predicted that prices will bounce back in August or September since the world's major central banks have already eased monetary policies recently.

"Traditionally, the oil demand is relatively low in the second quarter," Qu added, saying the bottom of oil prices may be reached in the third quarter. "When the demand traditionally goes up in the third quarter, the prices will start to go up."

(Cover: VCG)