- Home

- China

- World

- Asia-Pacific

- Americas

- Europe

- Middle-East and Africa

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

- Learn Chinese

Share

Copied

Homeless people wait for food during the lockdown in Dhaka, Bangladesh, July 14, 2021. /Getty

Editor's note: Risto Rönkkö is a research assistant at UNU World Institute for Development Economics Research (UNU-WIDER). Stuart Rutherford is founder of Shohoz Shonchoy, a microfinance cooperative. Kunal Sen, a professor at the University of Manchester, is director of UNU-WIDER. The article reflects the author's opinions and not necessarily the views of CGTN.

Even as rich countries begin to glimpse the light at the end of the pandemic tunnel, developing countries are struggling to contain COVID-19. But there are important lessons from the past year that can help governments devise more effective policies and programs to support their poorest residents amid continued outbreaks and lockdowns.

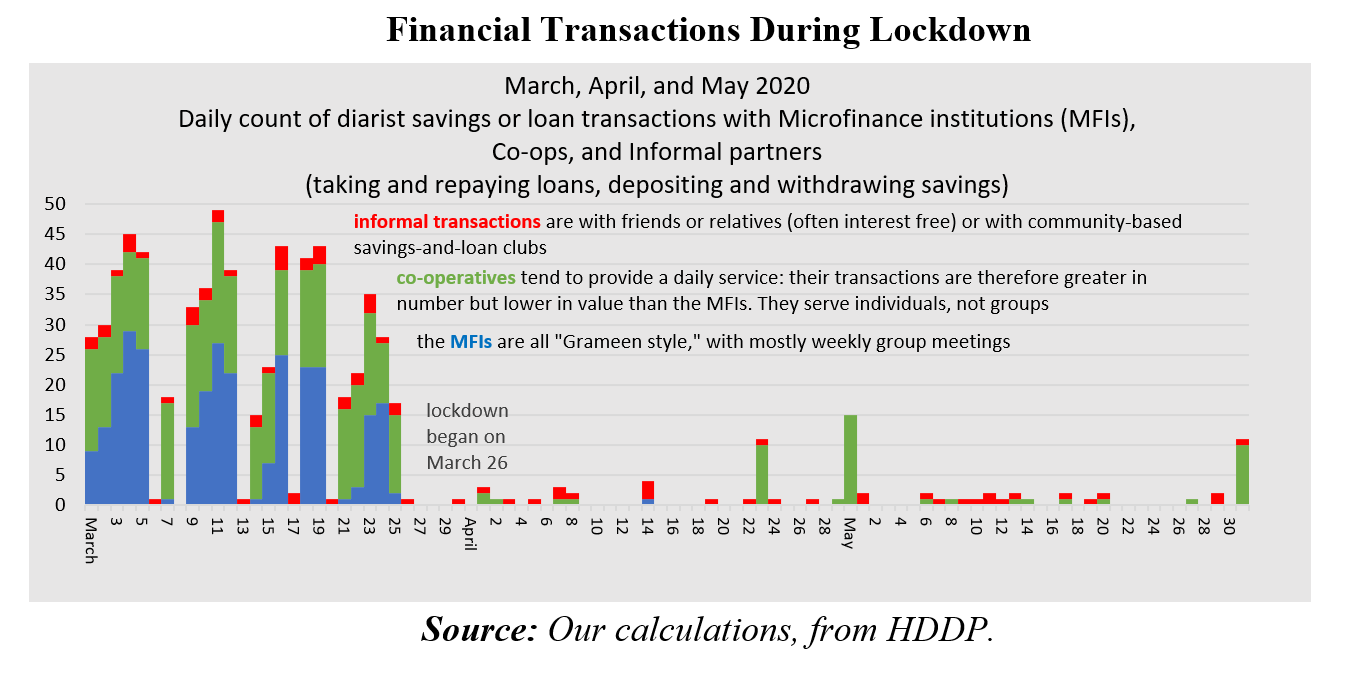

One valuable source of such lessons is the Hrishipara Daily Diaries project, which has been tracking the daily financial transactions of 60 poor households in rural Bangladesh for the last six years. Analysis of the data collected – especially the changes in spending patterns that have occurred during the pandemic – reveals four areas where governments should step in.

First, ensuring access to emergency cash. The rural poor are no strangers to shocks to their livelihoods. Droughts and floods are recurrent features in their lives, as are serious illness and job losses. But they usually have some access to lifelines: They can tap into family-based mutual-aid networks or borrow from microfinance institutions, money lenders, and friends and family.

That was not true during the COVID-19 pandemic. Restrictions on movement meant that households could not visit extended family to seek financial support. And even if they could, with everyone's livelihoods squeezed at the same time, friends and family often had nothing to offer.

Harsh lockdowns in many places also forced microfinance providers and other financial institutions to close, preventing households from borrowing or even withdrawing their savings. The 60 households in the study halted almost all financial transactions during the government-imposed lockdown.

This highlights the urgent need for large-scale unconditional cash transfers from the state, disbursed directly to the poor with minimal paperwork. A crisis of this magnitude is no time for fiscal rectitude.

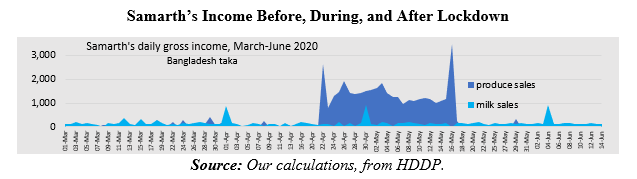

Second, poor people's capacity to exercise agency and entrepreneurial spirit should be supported. The project households were agile and resourceful in their response to the COVID-19 shock, and showed impressive money-management skills.

Sometimes this took an entrepreneurial form. For example, Samarth, a farmer who grows crops and rears dairy cows on a tiny parcel of land, quickly recognized that barriers to road transport were driving up prices of goods from the capital, thereby driving down the prices of local produce that was usually exported. So, he bought produce from desperate local farmers at very low prices and sold it at a temporary street market he set up inside Hrishipara. Local people, confined to their neighborhoods, provided the demand, and Samarth ended up with a major boost to his daily income during lockdown.

Policymakers rarely account for such entrepreneurial instincts in devising programs to support the poor. This should change, with policies that encourage and reward these instincts – and improve poor households' ability to harness them. For example, low-income households could be brought into consideration when devising "ease of doing business" regulations.

The private sector also has a role to play. In particular, the financial sector should develop flexible products that enable poor people to take advantage of opportunities that come their way. Of course, this also requires that governments ensure uninterrupted access to financial services during lockdowns.

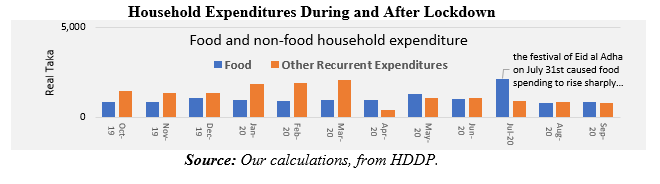

Third, the poor need generous food aid, especially during lockdown. Even under the most difficult circumstances, the project subjects found ways to put food on the table, but at the cost of drastic cuts in other expenditures. Our analysis shows a sharp reduction in recurrent household expenditures other than food in the first month of lockdown (April 2020).

Moreover, it was only in October – several months after lockdown ended – that those expenditures returned to pre-pandemic levels.

Finally, low-income households' cash reserves need to be protected. Most of the project subjects kept some cash at home for emergencies. The COVID-19 pandemic – and especially the lack of access to savings – meant that they kept those reserves to buy food and meet other basic needs.

The government and the financial sector should find ways not only to help secure these home-based reserves, but also to make it easier for the poor to replenish them. Expanding the scope of cash disbursements and making delivery more efficient is vital, as is keeping mobile-money agents open during crises.

The Hrishipara Diaries show that during COVID-19 lockdowns, the poor had to fend mostly for themselves. Thanks to their ingenuity, money-management skills, personal networks and past crisis planning, they managed to survive. But they also had to make great sacrifices.

As governments devise strategies to support the poor not only during COVID-19 lockdowns but also in future crises, they should reflect on what happened to the Hrishipara households during the pandemic so that next time, such sacrifices will not be needed.

Copyright: Project Syndicate, 2021

(If you want to contribute and have specific expertise, please contact us at opinions@cgtn.com.)