Business

16:23, 10-Dec-2018

China trade, inflation data indicate sweet spot for bond market

Updated

15:20, 13-Dec-2018

Share

Copied

Editor's note: Jimmy Zhu is a chief strategist at Fullerton Markets. The article reflects the author's opinion, and not necessarily the views of CGTN.

Chinese economic data released over the weekend, covering trade and inflation, paints a picture of its sovereign and high-grade bonds outperforming many other asset classes in the coming months and quarters.

Challenging external environment as synchronized global growth slowdown emerges

Export growth only rose 5.4 percent on a year-on-year basis in November, far below a 15.6 percent rise in October. The two factors behind the slower export growth are likely to extend into next year.

First of all, export orders are likely to decelerate after most front-loading activities come to an end.

Chinese exports to the U.S. grew 9.8 percent, a single-digit gain for the first time since April when U.S.-China trade tensions were just beginning.

Surprisingly, China's outbound shipping activities to the U.S. have accelerated since then.

Still, U.S. ISM manufacturing PMI new orders have been slowing in this period, which well explains why many Chinese exports to the U.S. can be categorized as front-loading.

When many U.S. buyers may have already shifted their future purchases to an earlier date, buying activity is set for a slowdown in the coming months regardless of the outcome of trade negotiations.

The second factor is that a synchronized slowdown in global activity looks inevitable after a multi-year recovery, as major central banks withdraw policy support.

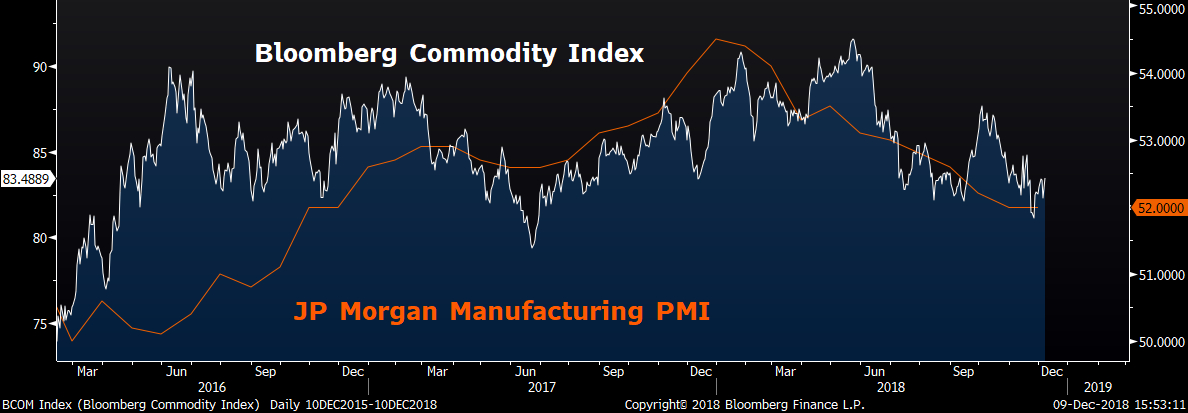

JPMorgan global manufacturing PMI has dropped to its lowest level since November 2016, and the Bloomberg commodity index is heading for its first yearly decline in three years. Major bond markets, including the U.S., Germany, and Japan, have all seen substantial gains since the beginning of the fourth quarter, showing investors are betting on an unfavorable global outlook in the coming months.

Furthermore, growth activities are likely to stay subdued as many companies may put their business plans on hold until the result of the U.S.-China 90-day negotiation period.

Source: Bloomberg

Source: Bloomberg

Growth in Chinese imports from the U.S. sees biggest decline since 2000 (Chinese New Year period excluded)

China's November imports grew 3.0 percent on a year-on-year basis, down from 21.4 percent in October, at the slowest pace since October 2016.

Slower imports, together with falling manufacturing PMI, reflect how domestic demand remains a concern.

China's imports from the U.S. are probably worth highlighting.

Imports from the world's largest economy tumbled 25 percent last month, the biggest decline since 2000 if excluding those months in the Chinese New Year period.

Import data shows that some Chinese importers started to look to other markets rather than the U.S., and this was likely a cause of the big drop in U.S. imports.

Chinese imports from the U.S. accounted for 8.46 percent of all of its global imports in 2017.

That number dropped to 7.95 percent in the second quarter this year and further declined to 7.06 percent in August.

In contrast, the portion of Chinese imports coming from emerging markets have been increasing in this period, and this may well explain why moves in the Chinese economy have become more relevant to emerging markets' assets.

However, the chart below shows that China's domestic demand is closely linked to its purchases from the U.S.

Correlation between China manufacturing PMI new orders and its imports' growth from the U.S. stands at 69.6 percent in the last three years.

Hence, a large drop in purchases from the U.S. signals waning domestic demand, possibly calling for more aggressive pro-growth support, especially with an increasingly fragile external environment.

Source: Bloomberg

Source: Bloomberg

The baseline scenario is that the possibility for China's central bank to cut its benchmark lending rate in the next 12 months shouldn't be ruled out.

Inflation data released over the weekend pointed to a similar outlook, with both CPI and PPI data further moderating.

Source: Bloomberg

Source: Bloomberg

When the Fed's chief Jerome Powell hinted that the current U.S. policy rate is just right below its neutral rates, anticipation for the People's Bank of China to be more proactive has been increasing. China's 10-year sovereign bond yield may have the scope to drop towards 3.05 percent in the next three months.