Business

18:50, 30-Nov-2018

PBOC may increase monetary support after PMI reaches critical point

Updated

17:48, 03-Dec-2018

Share

Copied

Editor's note: Jimmy Zhu is a chief strategist at Fullerton Markets. The article reflects the author's opinion, and not necessarily the views of CGTN.

China's November factory PMI points out that domestic demand is yet to find a bottom after recent policy support. Some more aggressive pro-growth measures could be needed in the coming months to support economic activities, including benchmark policy rate cuts potentially on the cards.

Three reasons behind November's factory PMI drop

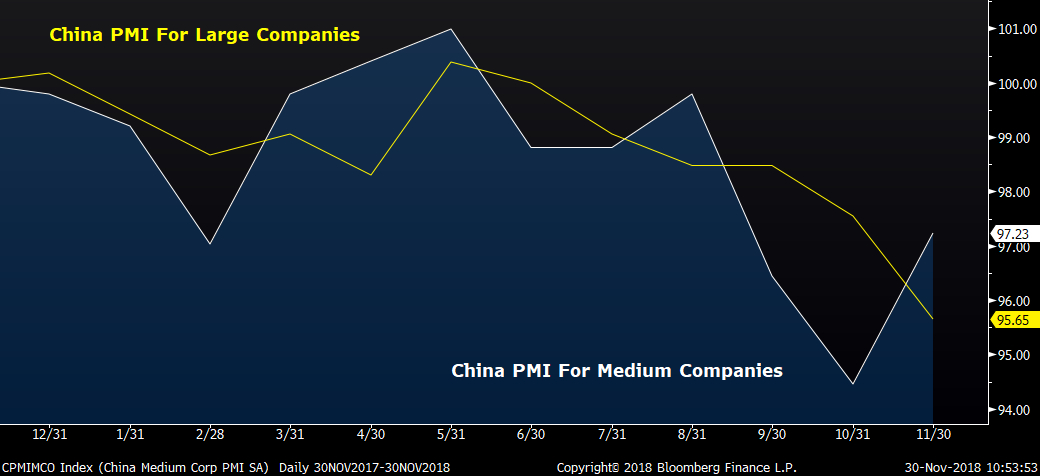

The headline manufacturing PMI figure has fallen to the key threshold level at 50.0, signaling factory activity this month is at its slowest pace in more than two years. Available data shows that there are mainly three factors behind the soft manufacturing PMI data. First of all, lower commodity prices have significantly knocked profitability for companies in upstream industries, which include many larger enterprises.

Thomson Reuters CRB Commodity Index slid 4.5 percent this month, its biggest decline since January 2016.

However, the falling prices increase profitability for small-medium enterprises, as most of them run downstream operations. China PMI for medium enterprises rose to 49.1 from 47.7 in the previous month.

Source: Bloomberg

Source: Bloomberg

Secondly, slower activity in the property sector continued to weigh on factory activity this month, reflected in the non-manufacturing PMI construction business activities index.

The index slid 4.6 points, its biggest drop since the index was made available in May 2012, to 59.3 points. This data has been largely consistent with property investment growth, which has been in contraction territory since the end of the first quarter this year.

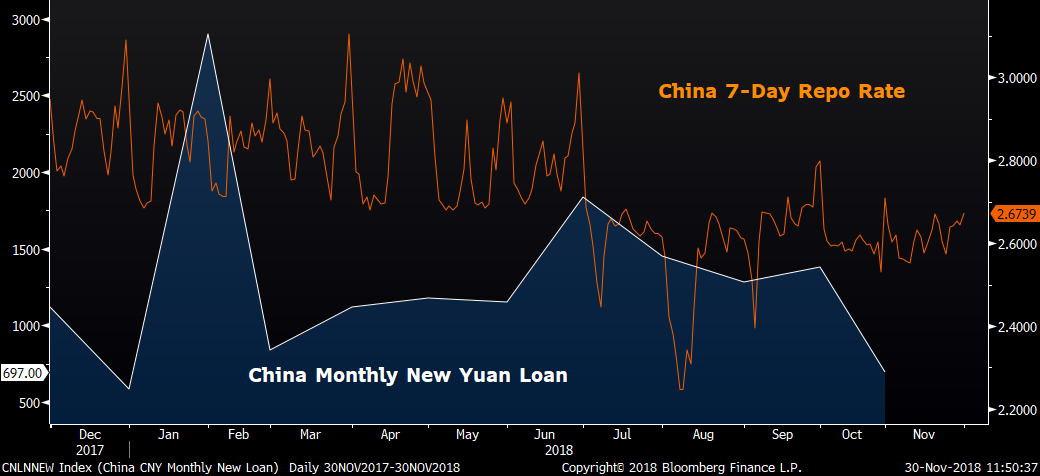

Recent credit data suggests the slowing housing activity may last for some time. New yuan loans dropped to 697 billion yuan in October, the lowest reading for the year so far, falling by almost 50 percent from 1.380 trillion yuan in September.

Source: Bloomberg

Source: Bloomberg

Thirdly, domestic demand has been slowing further even after recent policy measures, including some RRR cuts and fiscal stimuli. The new order index dropped to 50.4, sixth-month consecutive drop, making it the longest losing stretch on record.

The steel industry PMI fell 6.9 points to 45.2, the lowest since June 2016. The steel sector serves as a key industry to gauge the nation's growth outlook, as many industries in China are linked to this sector.

Fed hints that its rate hike may take a pause in 2019, which may increase the PBOC's policy flexibility

In past years, the PBOC has refrained from cutting borrowing costs or implementing similar measures, partly because the U.S. Fed has been in a tightening cycle since late 2015.

Things may start to change from now. After various dovish messages from the Fed this week that its current tightening cycle could have already approached a matured stage. Fed chair Jerome Powell said on Wednesday that the current Fed fund rates are "right below" the neutral level.

One day after Powell's speech, FOMC minutes signaled that the Fed will start to adopt a more flexible approach in gradual interest rate increases after a likely December hike.

The Fed ended its previous tightening cycle in June 2006, and since then China-U.S. 10-year government bond yields started to widen.

That being said, further narrowing between the two countries' bond yields is limited if the Fed starts to consider ending its current tightening cycle. That would increase monetary flexibility in China, by allowing the PBOC to set its policy to be more domestically focused.

The Chinese central bank has been injecting cash liquidity throughout the year, by cutting the RRR four times this year.

However, data shows that the policy effect hasn't effectively transmitted into the real economy.

China's seven-day repo rate has been climbing since the beginning of August, indicating that borrowing costs are rising.

At the same time, the growth of bank loans has decelerated. To spur domestic demand, policymakers may need to start considering lowering benchmark interest rates to reduce borrowing costs for both companies and consumers.