Money Stories

21:37, 08-Mar-2019

China to ease financing difficulties for SMEs

Updated

18:55, 09-Mar-2019

Share

Copied

05:26

The fall of popular Chinese bike-sharing startup ofo has left thousands of people looking for other ways to move around. Recently, live startup Panda Live went broke for the same reason, a rupture in the capital. In China, tens of millions of small-and-medium-sized enterprises (SMEs) like these contribute largely to the country's economy, innovation and employment, but many struggle to get decent loans.

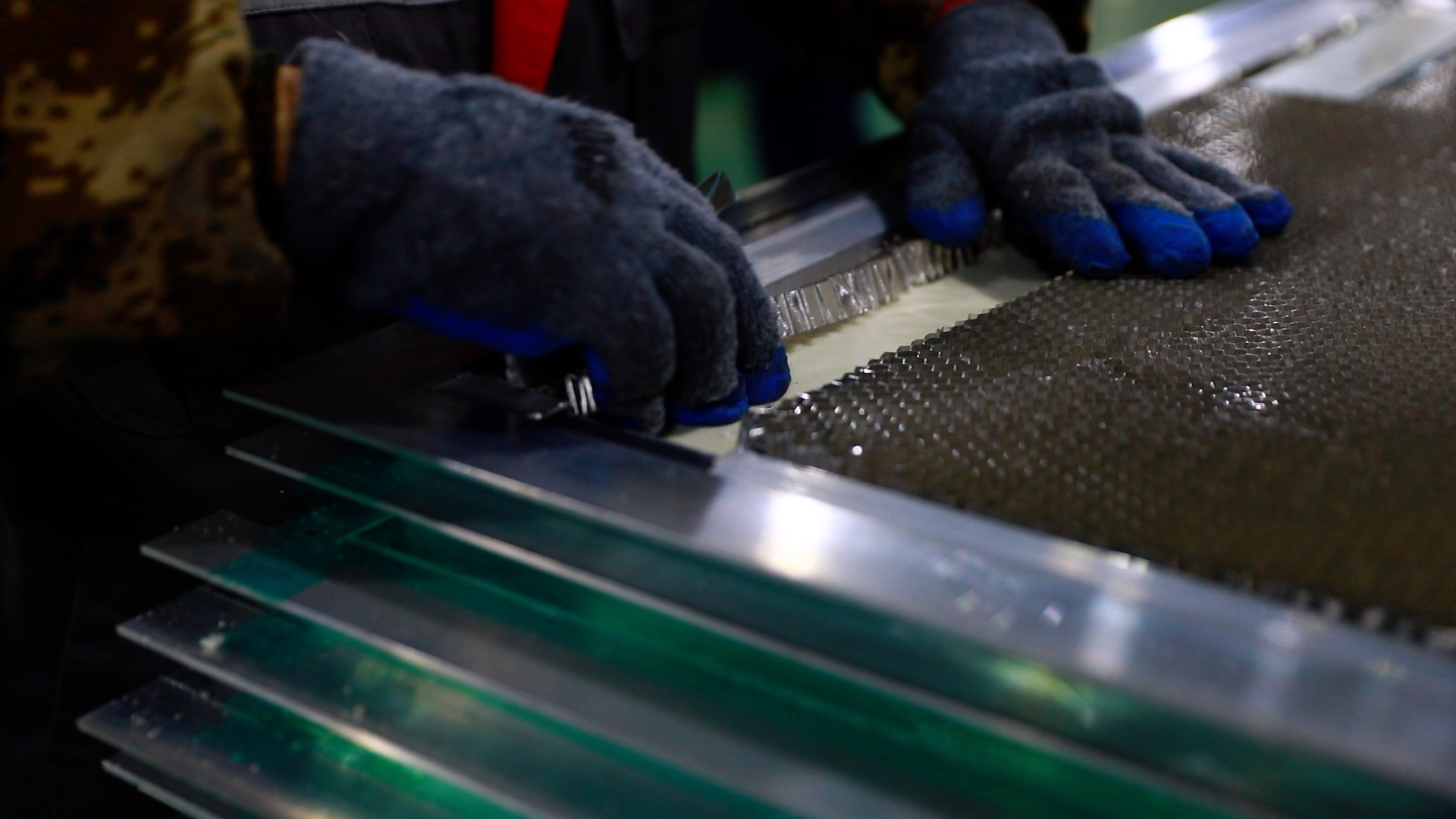

Yang Ning owns a company which produces ancillary facilities like honeycomb structures for railway vehicles in northeast China's Shenyang. He told CGTN that they've been growing fast amid China's railway development but have long faced difficulties in getting bank loans to expand their business. Without much tangible property for mortgage loans, they have tried various banking products but get very few results.

A worker making honeycomb structures at Yang Ning's factory /CGTN Photo

A worker making honeycomb structures at Yang Ning's factory /CGTN Photo

This is not an isolated case in China. Nearly nine out of every ten small companies are reported to have trouble getting money from financial institutions. Many still rely on private lending, and some even end up in debt traps. Song Biao, head of Shenyang's SME association, thought the stigma that SMEs' have poor credit, bad operations and a short corporate life cycle is a long-standing hurdle to financing.

Song said local authorities had taken many measures, like setting loan guarantee platforms and bridge loan funds, to change the situation somewhat. “But it helped only a few companies. Direct funds from government can hardly fill the big demand,” he added.

Yang's firm is lucky. Preferential policies will soon allow him to use his "honeycomb" patent as intangible property to borrow from the bank. The local government's intellectual property office, financing guarantee companies, and the Industrial Bank have come together to share the risk.

Yang hailed it as a breakthrough in corporate financing. Once in place, it can bring his firm five to eight million yuan in the short term. “That's a small amount but very important to our working capital, and it keeps us viable," Yang said

While China's central government calls on banks to increase their lending and lower thresholds for small enterprises. Pan Lei, an Industrial Bank branch manager, said they are pushed to improve their financial services, which deal with conditions that traditional products cannot cover.

Potential borrowers at the bank counter /CGTN Photo

Potential borrowers at the bank counter /CGTN Photo

Pan said new attempts are aimed at SMEs' particular operation features and financing needs. “For example, other than solutions for tech companies, we also develop supply-chain financing services for trading companies without collateral. That is, we trace capital, material and information flow between the borrower with its core business partner- trusty companies on the supply chain- to make sure the firm is doing okay,” Pan explained.

But lenders have their own worries, namely, whether companies use the money to conduct regular business rather than speculate on the market, and whether and how they can repay the loans. The banker said small business lending lacks solid information.

At the annual meeting of China's top legislature, some delegates addressed the issue.

Xu Liyi, the mayor of Hangzhou, said the government should take the lead to build a credit system that combines information of taxpaying, employment, fees and much more with big data technology apart from providing guarantees and incentive mechanisms. He mentioned that the city of Hangzhou, home to tech giants like Alibaba, has done a lot in this area, but still has a long way to go to widely serve financial institutes.

Liaoning Equity Exchange Center /CGTN Photo

Liaoning Equity Exchange Center /CGTN Photo

In the central government's recent work report, Premier Li Keqiang admits that challenges of SME financing remain. Authorities will continue to roll out monetary policies to funnel capital to small businesses, and a goal is set for big state-owned commercial banks to increase their loans to small firms by over 30 percent year-on-year in 2019. Meanwhile, the nation's top regulators also note that more work should be done in other financial sectors, in addition to banking.

China is determined to make full use of direct financing methods, like regional equity markets, insurance, bond and venture capital, to better support the growth of small enterprises. And that may require a bit of innovation. For example, Yang has listed his manufacturing company at the local equity exchange center. The manager expected to get some 20 million yuan with equity pledges in the long run.

However, experts say the core of the financing dilemma remains the vitality of small businesses. After all, who would dare lend with no hope of payback?

Shenyang's SME Association chairman believed timely payments could be more helpful than loans for SMEs suffering from cash flow gaps. "And we will also strive to raise our competitiveness in the market and work together towards fair and transparent deals," he said.

Efforts to improve the overall business environment are also on the agenda. As for Yang, he will soon benefit from a new round of tax relief on manufacturing and transport corporates groups. With additional support for rising companies in backbone industries, despite the critical financing situation, he has faith in making more honey out of his “honeycombs".