Biz Analysis

18:28, 21-Mar-2019

Fund manager portfolios need reshuffle after Fed meeting

Share

Copied

Editor's Note: Jimmy Zhu is chief strategist at Fullerton Research. The article reflects the author's opinion, and not necessarily the views of CGTN.

The U.S. Federal Reserve's latest dot plot suggests there won't be any rate hikes in 2019, and its balance sheet unwinding will end in September.

However, the clear direction is puzzling investors -- does looser monetary policy mean they should favor riskier stocks or safer bonds? The answer seems to be clear if the Fed's prediction on inflation is accurate.

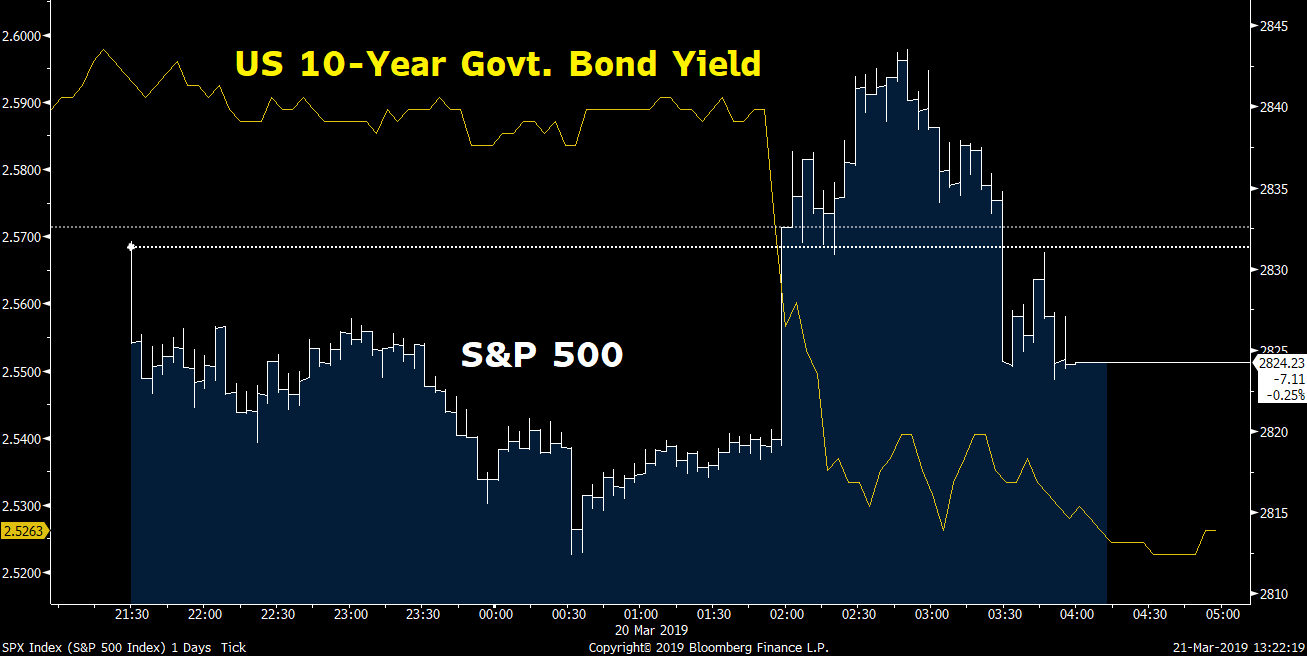

The immediate reaction in the market showed that traders were buying more bonds than stocks. The chart below shows the S&P 500 initially climbed when the Fed's statement was released, but quickly pared all gains after Fed Chief Jerome Powell expressed his concerns on slowing global growth and domestic inflation. The U.S. 10-year sovereign bond yield dropped eight bps, the biggest decline in nine months, to 2.52 percent.

Source: Bloomberg

Source: Bloomberg

One of the key reasons behind the Fed's hold on rate increases is its inflation outlook, with the effect of last year's tax reforms diminishing. The latest monthly survey conducted by the New York Fed showed inflation at 2.8 percent, down from 3.0 percent in January. If the Fed's prediction on inflation is accurate, U.S. bond yields have further room to slide.

The chart below shows that U.S. CPI and the 10-year government bond yield have been moving in tandem since 2000, with correlation at 0.66 in the past five years. Based on our regression analysis, current U.S. CPI at 1.50 percent on a year-on-year basis means the U.S. 10-year government bond yield should be at 2.32 percent, another 20 bps lower than the current 2.52 percent.

Source: Bloomberg

Source: Bloomberg

On the other hand, the average spread between the U.S. CPI and its 10-year government bond yield in the past five years stood at 64 bps, much narrower than the current 100 bps spread. This also means that the bond yield may further decline and converge with the inflation rate.

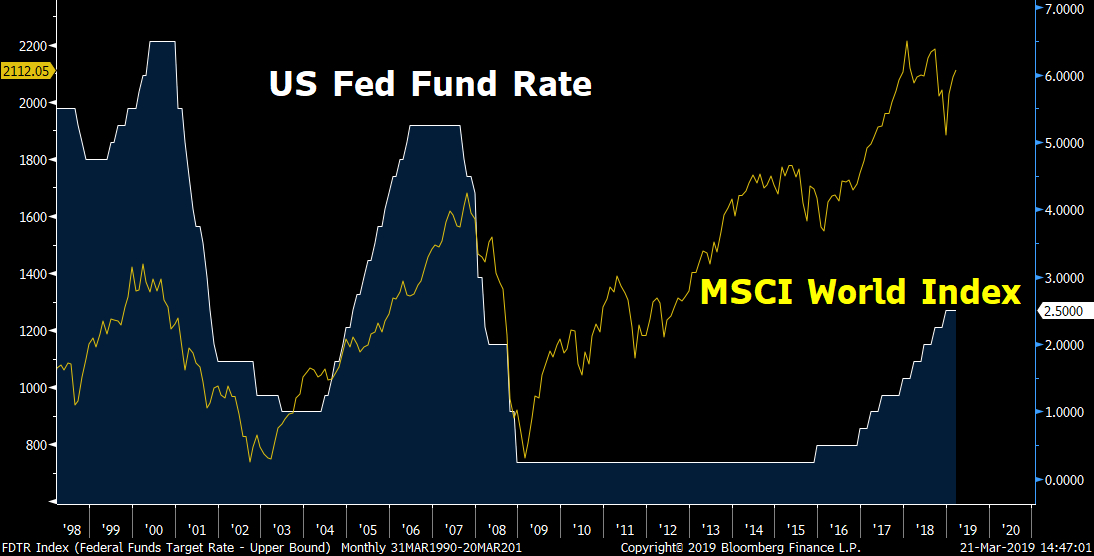

A dovish Fed is usually welcomed in the stock market, but historical data suggests that might not be the case this time. If we assume the current Fed fund rate is near the level of the neutral rate, global stocks may be approaching a peak.

The chart below shows that global stocks fail to edge higher once the Fed decides to end its rate hike cycles. When the Fed ended its tightening cycle in May 2000, the MSCI world index had peaked two months earlier. The Fed ended another round of tightening in June 2006, and again the MSCI world index peaked within the next 12 months.

Source: Bloomberg

Source: Bloomberg

It is also worth mentioning that easing cycles have always arrived shortly after the Fed putting an end to its tightening cycles. The Fed cut its benchmark rates in January 2001, seven months after it stopped raising rates.

The Fed also reduced its benchmark interest rate a year after ending a rate hike cycle in 2006. The futures market shows a rate cut probability of 49.4 percent in January 2020, following the latest FOMC meeting.

Most investors expect the Fed's easing cycle to favor stock prices, thanks to increasing liquidity. But the chart above shows global stocks get sold off during Fed easing cycles. The MSCI world index slid around 40 percent when interest rates were cut from 2001 to 2003, and global stocks tumbled over 50 percent in the Fed's next easing cycle.

Although we don't expect the Fed to lower its interest rate in the next 24 month period based on the current backdrop of the U.S. economy, a sudden pull back of the FOMC's rates projection has sent a valid warning about the strength of the global economy.

Asian stocks were mixed during Thursday's trading session, as the gloomy outlook may have prompted some investors to take profit.

As of Thursday, the MSCI world index has rallied over 12 percent since the end of 2018, while the Bloomberg Barclays global aggregate bond index is only up 1.7 percent. The outcome of the FOMC March meeting may encourage some investors to shift their portfolio back towards bonds.