Business

08:53, 09-Aug-2017

Internet titans’ ambition for a cashless China

Share

Copied

“In five years, we will make most of the cities cashless societies in China. Hangzhou, my city, is already a cashless society, almost,” Jack Ma, founder and executive chairman of China’s e-commerce giant Alibaba Group, made an ambitious claim during the group’s Gateway 17 Conference in Detroit in June.

Alipay, the mobile payment tool run by Alibaba’s affiliate Ant Financial, is making all efforts to implement Ma’s plan in an escalating competition with rival WeChat Pay, the other major third-party payment tool under Chinese Internet titan Tencent Holdings Ltd.

Cashless Society Campaign

Alipay launched a campaign named “Cashless Society Week” from August 1 to 8 to encourage users to replace cash in all transactions in the week with Alipay.

Of course, award money and coupons, which are Chinese Internet companies’ talisman in recruiting users, are offered in different amounts for each transaction.

A stand owner in a grocery market in Wuxi city, eastern China’s Jiangsu Province offers Alipay and WeChat Pay QR codes for customers to pay. /VCG Photo

A stand owner in a grocery market in Wuxi city, eastern China’s Jiangsu Province offers Alipay and WeChat Pay QR codes for customers to pay. /VCG Photo

The campaign effectively expanded its influence in wider audiences and areas. The number of mobile transaction made by users at and above 50 years old surged about 10 folds year-on-year and the transaction number out of tier-1 and 2 cities jumped 10 percent year-on-year, according to data Ant Financial sent to CGTN Tuesday.

Meanwhile, Alipay’s rival competitor WeChat brings enormous pressure when the latter enjoys fast growth thanks to WeChat being China’s most widely-used instant messaging app.

In fact, WeChat initiated a “Cashless Day” campaign back in 2015. This year, when Alipay announced the “Cashless Society Week,” WeChat claimed to expand its cashless campaign to the whole August and invited as much as offline shops to join in.

Others swipe, we scan

Unlike many developed economies’ high penetration of credit cards or bank checks, China seems to have stepped over the period and become a stunning leader in digital payment with a dramatic surge in a short time.

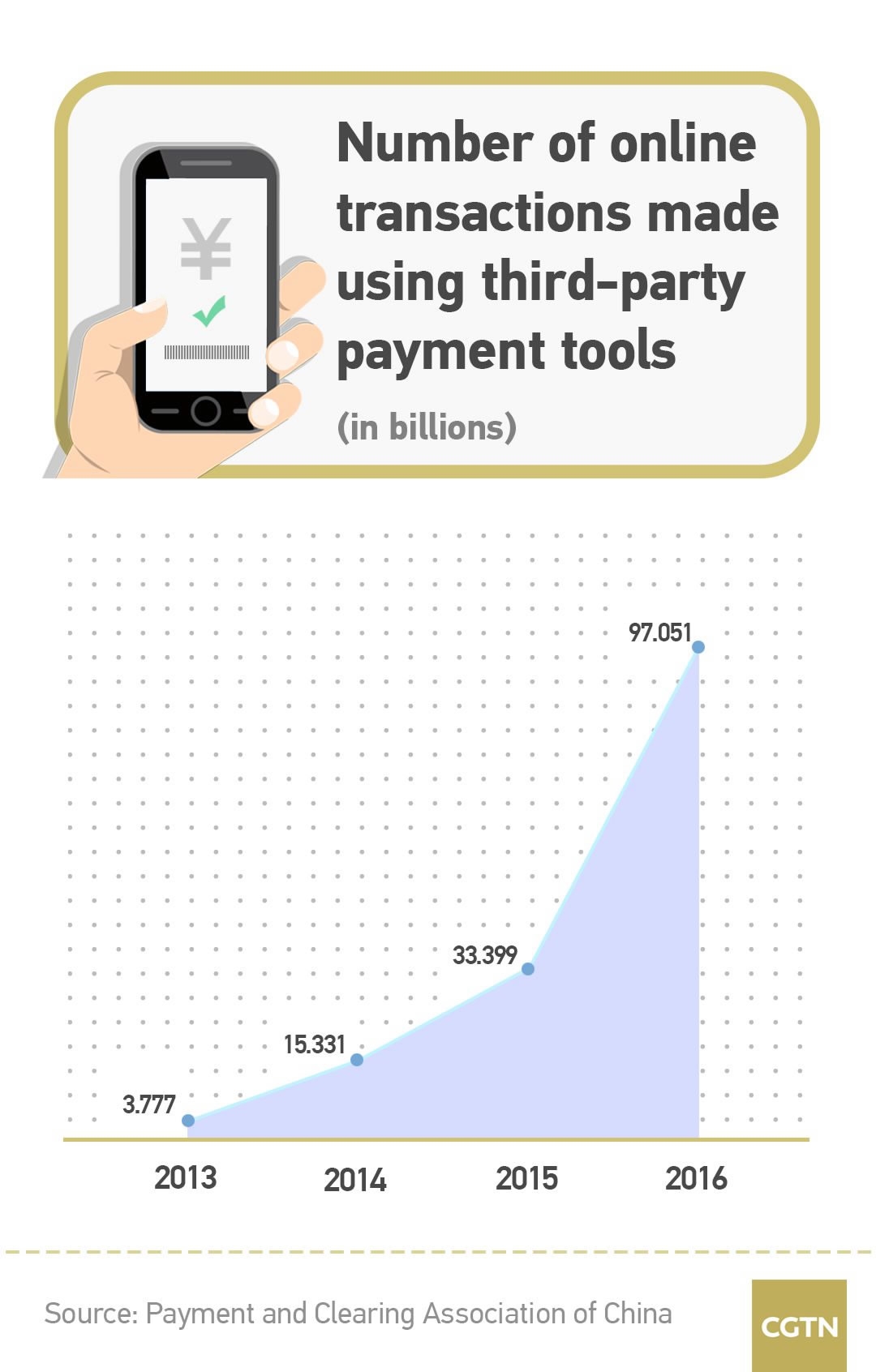

In only three years from 2013 to 2016, the total number of mobile transaction via the third-party payment platforms skyrocketed more than 30 folds from 3.77 billion to more than 97 billion, according to official data from Payment and Clearing Association of China.

Chinas’ mobile payment reached 5.5 trillion US dollars in 2016, almost 50 times of the size of US market 112 billion US dollars in the same year, according to data from consulting firm iResearch.

The huge digital payment market has been carved up mainly by Alipay and WeChat Pay with 54 percent and 40 percent respectively in the first half of 2017, another iResearch report showed.

But they adopted the same strategy: involving the end-users into its business ecosystem as deep as possible. The two payment tools can complete every single transaction in your life: purchasing online or offline, hailing a car, booking a flight or train ticket, topping up your phone, paying utility bills, transferring money to every account and even buying various wealth management products.

Regulation to catch up

Nothing is perfect, neither is digital payment.

Currently, the online payment via the third-party payment tools in China are conducted directly between the payment tools and banks, bypassing the central bank’s clearing system.

So the central bank could not have detailed transaction information and capital flow and there are rising concerns that the direct payment tools-bank connection can be used in money laundering, credit cards cashing out and illicit money transferring.

Therefore, the People’s Bank of China, the country’s central bank, has required all banks and third-party payment institutions to connect to a unified platform called Nets Union Clearing Corporation (NUCC) by June 30 of 2018 to ensure effective regulation and transaction security.