- Home

- China

- World

- Asia-Pacific

- Americas

- Europe

- Middle-East and Africa

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

- Learn Chinese

Share

Copied

The logo of JD Logistics. /CFP

The successful debut of JD Logistics (JDL), the logistics arm of e-commerce company JD.com, on the Hong Kong Stock Exchange on Friday is expected to change the competition landscape of the logistics red ocean in China.

With the proceeding of $3.2 billion raised, JDL said it will focus on upgrading and expanding its logistics networks – including last mile and longer distance lines as well as cold chain and bulky item networks, developing supply chain technologies and overseas expansion.

In recent years, the company has shifted its business strategy from serving as JD.com's in-house delivery segment to expanding businesses to cover more external customers.

This will further escalate the competition in China's logistics sector, Sun Xiaotian, analyst from research team of Nasdaq-listed Futu Holdings said, adding that there will be a few giants coexisting in China in the future, as no single company could take the whole market.

The JDL's IPO is the third mega listing for the JD empire over the past year, adding to the U.S.-listed Chinese tech firms' "home-coming" trend to Hong Kong amid continuing tensions between Beijing and Washington.

JD Health, healthcare arm of JD.com, was listed in Hong Kong last December raising $3.5 billion. The parent U.S.-listed JD.com made a secondary listing in Hong Kong in June 2020, following the secondary listing of main rival Alibaba under the new listing regime of the city.

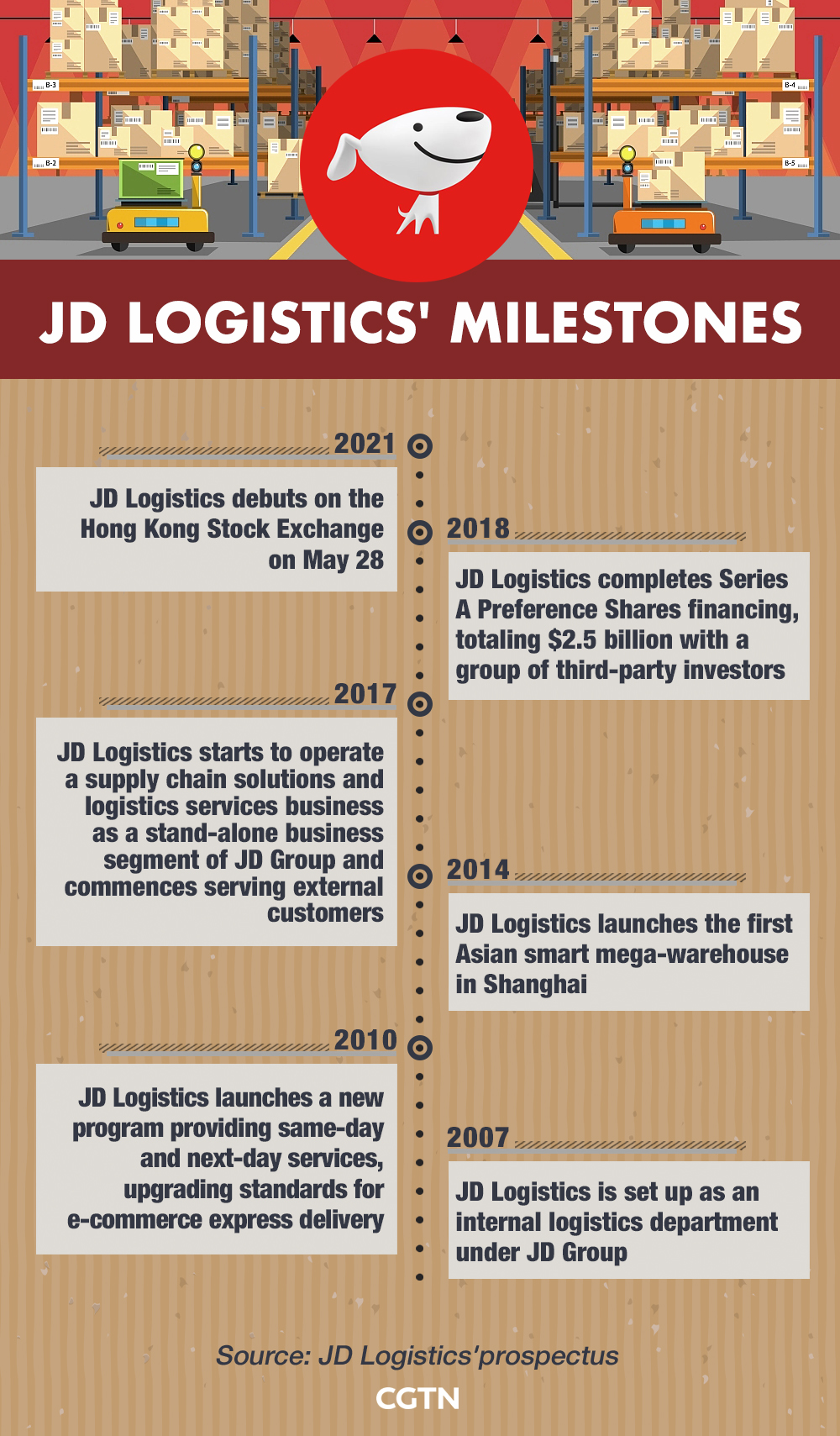

JDL was set up as a separate unit in 2007 by JD.com in order to differentiate from its competitors in China's cut-throat e-commerce market, serving its growing supply chain and timely logistics demands.

Before 2017, the unit remained an internal part of JD.com's e-commerce operations; but later was spun out and started offering services to third-party retailers. In 2018, it started serving external consumers with a new parcel delivery demand.

JDL positioned itself as an "integrated supply chain logistics services provider" controlling a market share of 2.7 percent in terms of total revenue in China's integrated supply chain logistics services industry in 2020, being strong in warehousing and logistics technology.

The Chinese delivery and warehousing firm has been focusing on the same-day and next-day deliveries, which has leveled up the standards of e-commerce express delivery.

'Cat-and-dog' fight continues

The fierce battle among e-commerce players, such as JD.com and Alibaba, will extend to the logistics sector, Southwest Securities Analyst Chen Zhaolin wrote in a report.

In 2013, JD.com's main rival Alibaba launched a logistics network, Cainiao, with eight other traditional third-party logistics (3PL) companies, including Shentong, Yuantong, Zhongtong, and Yunda.

JDL has better logistics timeliness and stability of services given its wider self-build warehouses while Cainiao has a broader scope of regional logistics integration with more flexible operation, Chen said.

Meanwhile, JDL faces competition not only with Cainiao but also traditional 3PL companies such as the market leader SF Express.

E-commerce logistics companies represented by Cainiao and JDL have traffic endowments from their parents' platforms, Chen said, but their networked distribution capabilities are slightly weaker than big 3PL companies.

"As there is no clear sphere of influence among the logistics giants. Therefore, Cainiao, JD.com, and SF Express will be in a state of competition and cooperation for a long time," he added.

Unpredictable prospects

To fulfill its timely logistics services, JDL took a relatively asset-heavy path, spending huge investments on automated logistics warehouses and possessing intensive labor.

The prospectus said the company has operated more than 900 warehouses across China, with a total storage area of approximately 21 million square meters, and over 190,000 employees are engaged in delivery.

Chen cautioned that the prospects for growth of JDL are unclear, pointing out that the effect of the JD logistics scale has not yet been reflected in economic efficiency and labor costs take the bulk of its total costs.

The company is still loss-making – figures in the prospectus showed a net loss of 4.1 billion yuan ($642 million) last year.

While accelerating warehousing construction under the strategy of promoting the logistics upgrading in low-tier cities, JDL may encounter a dilemma to create profits, Chen said, adding that its insufficient price attractiveness directly affects the volume of orders.

Low-tier cities are highly sensitive to logistics prices, and the high costs of JDL to improve its timeliness will inevitably need to be offset by intensive orders and relatively higher services charges, he explained. In contrast, the Alibaba-backed logistics network provides lower-priced logistics services with the support of 3PL's scale effect.

In addition, labor costs are key factors that can't be underestimated for JD Logistics profitability, Chen said, citing concerns over labor-intense strategy to maintain high services quality and the natural increase in labor costs.

The logistics network that JDL has built is at the core of its competitiveness, Sun said, stressing that the company "will have to largely expand revenue from external customers to be profitable."

From 2018 to 2020, JDL's total revenue from external consumers increased from 9.8 percent to 24.2 percent, the prospectus showed.

(Graphic by Gao Hongmei)